SST can be used to estimate a wide variety of models by the method of

maximum likelihood. The MLE procedure allows users to program their

own likelihood functions. For most purposes, however, users will want to

use SST procedures which have been preprogrammed for standard models, such

as the LOGIT, PROBIT, TOBIT, MNL, and

DURAT commands. These commands have roughly the same syntax as the

REG command and make it no more difficult to estimate a probit

model, for instance, than to run a regression.

The purpose of this chapter is to describe the various models

which can be estimated by SST and to explain how to execute the

appropriate commands. The discussion of the models is kept at a

fairly simple level and references are provided for more detailed

discussions about the statistical properties of the procedures.

The models discussed in this chapter fall within the category

of limited dependent variable models, as they are known in

econometrics. Logit, probit, and Tobit models, in particular,

can be thought of as extensions of the linear regression model to

situations where the dependent variable is limited: either the

dependent variable has been categorized (as, for example, when

responses are classified as "low," "medium," or "high") or else

some values are impossible (consumer expenditures, to cite one

example, cannot take on negative values). This type of model is

particularly relevant in the modelling of choice processes.

Econometricians have adapted the multinomial logit model for the

purpose of estimating "random utility models." SST makes the

estimation of random utility models particularly simple.

We focus initially upon models for dichotomous dependent

variables. These models are somewhat simpler to explain than

models for polytomous (multiple category) dependent variables

and, for some users, are all that is required. In the case of a

dichotomous dependent variable, the logit and probit models will

produce very similar results (the estimated coefficients should

be approximately proportional to one another, as described

below). For this reason, we discuss the so-called binary

models together.

When the dependent variable is polytomous, the LOGIT and

PROBIT commands, as implemented in SST, will produce rather

different output. The PROBIT command in SST is for an ordered

categorical model. This will be appropriate when the categories

of the dependent variable can be ordered in a natural way.

Survey responses often can be treated this way. For example, if

respondents are asked whether they "agree strongly," "agree

weakly," "disagree weakly," or "disagree strongly" with some

statement, then their responses can be ordered. The ordered

probit model in SST provides an alternative to arbitrary scoring

schemes of responses that would be required for regression

analysis.

The LOGIT command in SST is for unordered responses. A typical

example would be when an individual can choose from a set of discrete

alternatives. In transportation mode analysis, one may try to predict which

mode (e.g., car, bus, or train) an individual will pick. Since there is no

natural ordering of these alternatives, one approach would be to try to

estimate the probability that each alternative would be chosen. For this

purpose, the unordered logit model would be suitable. Later we also discuss

how random utility models can be used for this purpose (the MNL

command can be used for estimation of random utility models). These two

models are closely related. In fact, the MNL command can be used to

estimate unordered logit models as well as the LOGIT command, but it

is much more cumbersome to do it this way.

The TOBIT command is used to estimate censored regression

models and is most often applied to the analysis of expenditure

data. The DURAT command is used to estimate discrete time hazard

models (e.g., for analyzing spells of unemployment). They are

discussed later in the chapter.

The last section of the chapter discusses the MLE command

which computes maximum likelihood estimates for user-defined

models. The same procedure can be used for nonlinear least

squares estimation. The MLE command differs from the previously

mentioned commands in that the user must also specify the

derivatives of the log likelihood function, while in the other

commands these derivatives have been preprogrammed. Since the

algorithm used for the MLE command is slightly different from

that used for the other commands, the options available also

differ.

The method of maximum likelihood involves specifying the

joint probability distribution function for the sample data. We

assume that we have a random sample of size n drawn from some

probability distribution. Let Y_1 ... Y_n denote the random

variables that we sample. If the Y_i are discrete random

variables, then the probability that Y_i takes any particular

value y_i is given by the

probability mass function:

In general, f(y_i) will depend upon some unknown parameters

beta_l ... beta_K which we want to estimate. To indicate

the dependence of the probabilities on these parameters, we write:

The joint probability mass for the random variables Y_1 ... Y_n

is the product of the individual probability mass functions:

This is a function of both the values

y_1 ... y_n taken by the

random variables and the parameters

beta_1 ... beta_K. However, once a

sample has been drawn, the values taken by the random variables

are known. For any choice of the parameters beta_1 ... beta_K,

we can

evaluate the probability of obtaining the observed sample values:

where Y_1 ... Y_n are now fixed at their observed values. The

function L(beta_1 ... beta_K) is known as the likelihood

function. The basic idea of maximum likelihood estimation is to choose

estimates (beta hat)_1 ... (beta hat)_K so as to maximize the

likelihood function. The probability of observing the sample values is

greatest is the unknown parameters were equal to their maximum likelihood

estimates. This principle makes good intuitive sense and also turns out to

have a solid theoretical foundation.

If the data are continuous, rather than discrete, we simply

substitute the probability density function for the probability

mass function. Also, for most purposes it is easier to work with

the log of the likelihood function. Since the logarithm is a

monotone increasing function, log

L(Beta_1, ...., Beta_K) and L(Beta_1, ..., Beta_K)

will be maximized at the same values.

The method of maximum likelihood has several features that are worth

noting. Under relatively weak assumptions, usually called regularity

conditions, maximum likelihood estimates are (1) consistent, (2)

asymptotically normal, and (3) efficient. Consistency means that as the

sample size increases, the maximum likelihood estimate tends in probability

to the true parameter value. Moreover, for large sample size, the maximum

likelihood estimate will have an approximate normal distribution centered

on the true parameter value. The standard errors produced by SST are

"asymptotic standard errors" in the sense that they are large sample

approximations to the sampling variance of the maximum likelihood

estimates. Similarly, the t-statistics produced by SST maximum

likelihood procedures are "asymptotic t-statistics" in the sense that

they have an approximate t-distribution for large samples. There is no

hard and fast rule for how large the sample size should be for these to be

good approximations. An often-cited rule of thumb is thirty observations

(or thirty observations per parameter) are required before asymptotic

theory should be invoked. With large cross-sectional datasets, however,

sample sizes will be much larger than this, so the use of asymptotic

approximations will not be at issue. Finally, efficiency means that maximum

likelihood estimators will have smaller (asymptotic) variance than other

consistent estimators (technically, other consistent uniformly

asymptotically normal estimators). The theory of maximum likelihood

estimation is covered in most statistics texts. See, for example, C. R.

Rao, Linear Statistical Inference and Its Applications, 2nd ed.

(Wiley, 1973), chapter 5.

When the model is misspecified, then maximum likelihood estimators may lose

some of their desirable properties. However, it has been shown that under

very weak conditions, maximum likelihood estimators will still have a

well-defined probability limit and will be approximately normally

distributed. Moreover, it is still possible to compute the variance of

maximum likelihood estimators based on a random sample even if the model is

badly misspecified. The ROBUST subop to the maximum likelihood

procedures computes standard errors for maximum likelihood estimates that

are insensitive (or "robust") to model misspecification. For details, see

Halbert White, "Misspecification and Maximum Likelihood Estimation",

Econometrica (January, 1982). White suggests comparing the usual

and robust estimates of the covariance matrix of maximum likelihood

estimators as a test of model specification.

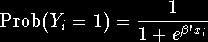

Suppose that the dependent variable takes only two values,

say zero and one. (SST does not care how your dependent variable

is coded; it treats the low value as if it were zero and the high

value as if it were one in this example. It is not necessary to

recode your dependent variable.) We will be interested in the

probability that the dependent variable takes the value one (the

high value). The probability that the dependent variable equals

zero is, of course, one minus the probability that it equals one.

Now probabilities are required to fall between zero and one, so a

linear regression model is not appropriate to the modelling of

probabilities since for extreme values of the independent

variables, the predicted value of the dependent variable will be

either less than zero or greater than one, which is impossible

for a probability. What is needed is a model that ensures for

all values of the independent variables, the predicted

probability of the dependent variable equalling one is

admissible.

Let Y_i denote the dependent variable and x_1i ... x_Ki

denote the independent variables. A reasonable choice of functional form

for the probabilities is:

where beta' x_i = beta_1 x_1i + ... + beta_K x_Ki and

F(.) is a nondecreasing function such that:

Any cumulative probability distribution function will satisfy these

conditions. Two distribution functions which have often been used are the

logistic:

and the normal:

PHI(.) corresponds to the SST function cumnorm. In

either case, if beta' x_i is large, then the probability that Y_i

equals one is close to one. Similarly, if beta' x_i is small, then

the probability that Y_i equals one is close to zero. Whatever values

the independent variables take, the probability that Y_i equals one

will be admissible (i.e., between zero and one).

When we specify F(.) to be logistic, then we have the

logit model. The log likelihood function for the logit model is given

by:

where F(t) denotes the cumulative logistic distribution function.

When we specify F(.) to be normal, then we have the

probit model. The log likelihood in this case is given by:

Both the logit and probit log likelihoods are globally concave and

hence relatively easy to maximize using the Newton-Raphson algorithm.

The LOGIT command uses an iterative nonlinear optimization procedure

to obtain parameter estimates that maximize the logit log likelihood

function. You specify the dependent variable in the DEPsubop and the

independent variables in the IND subop in much the same as the

REG command. Suppose, for example, that the variable y takes

only two values. In our examples, we will assume y equals zero or

one, but the LOGIT and PROBIT commands don't require this.

Then to obtain estimates for a binary logit model, type:

logit dep[y] ind[x1 x2 x3]

As in regressions, it is advisable to include a constant term in

the IND subop, though SST does not require you to do so.

The PROBIT command produces parameter estimates that maximize

this function. The syntax is identical to that for the LOGIT

command:

probit dep[y] ind[x1 x2 x3]

The same advice about including a constant term in the IND subop

applied here as well.

For the case that we have been considering (dichotomous

dependent variables), LOGIT and PROBIT will produce similar

results. The logistic distribution has variance (pi^2)/3 while the

standard normal distribution, of course, has variance one. This

means that the coefficients based on the binary logit

specification should be approximately sixty percent larger than those

based on the binary probit specification. (Multiplying the binary logit

estimates by sqrt(3)/pi makes them roughly comparable to the binary

probit estimates.) If the observations

are highly skewed, then the choice between the logit and probit

specifications may be of greater consequence, but this is a

rarity in most applications.

In either the LOGIT or PROBIT commands, SST allows the user

to save the predicted probabilities with the PROB subop. If the

dependent variable has two categories, then the predicted probability is

the estimated probability that the dependent variable takes its high

value. You should specify one variable name in the PROB

subop. Following our example above, where y takes the values zero and one,

we could give the LOGIT command:

logit dep[y] ind[one x1 x2 x3] prob[phat]

SST will compute the probability y takes its high value and save these

estimated probabilities in the variable phat. The ith

observation on the variable phat would be:

If the PROB subop is included with the PROBIT command, then

the estimated probability that y takes its high value is given by:

In either case, the estimated probabilities can be used to compute a

goodness of fit statistic, the percentage of cases correctly predicted. In

the binary logit and probit models, we would predict that a case would fall

into the category with the modal (highest) predicted probability.

That is, if Prob(Y_i=1) >= Prob(Y_i=0), then we would

predict that Y_i equals one, while if Prob(Y_i=0) >

Prob(Y_i=1), then we would predict Y_i equals zero. We

could then compare our predictions to the actual outcomes on the dependent

variable. The percent "correctly predicted" is just the fraction of cases

where the actual outcome corresponds to the "predictions" described above.

We describe this calculation in some detail for the probit model. The

calculations for the logit command are identical, except that we initially

use the LOGIT command instead of the PROBIT command.

First, we compute maximum likelihood probit estimates and

save the probabilities in the variable phat:

probit dep[y] ind[one x1 x2] prob[phat]

Next, we create a dummy variable which equals one if the case is

predicted correctly and equals zero otherwise:

set success = ((phat >= 0.5) & (Y == 1)) | ((phat < 0.05) & (y == 0))

Finally, we calculate the percentage of successes:

freq var[success]

The number produced is the "percentage correctly predicted". It

should be understood that while this statistic can be a useful

diagnostic, it is not really a "prediction" (since the actual

outcomes have been used to compute the probit or logit

estimates). Furthermore, the percent correctly predicted is

guaranteed to be fairly high, and will be very high if the

dependent variable is skewed.

As in the REG command, estimated coefficients and the

variance-covariance matrix can be saved using the COEF and

COVMAT

subops. The user supplies a variable name in each subop, and SST

stores the coefficient estimates or covariance matrix (stacked by

column) in the specified variable.

With the PROBIT command, the values of beta' x_i can be saved

for each observation by specifying a variable in the PRED subop.

This provides another route for obtaining predicted probabilities, since

the probability that the dependent variable takes its high value can be

obtained by evaluating the cumulative normal distribution function at

beta' x_i. Users may find this option helpful for performing selectivity

corrections (see James Heckman, "Sample Selection Bias as a Specification

Error", Econometrica, January 1979) or simultaneous probit

estimation (see L. F. Lee, "Simultaneous Equations Models with Discrete

Endogenous Variables", in C. Manski and D. McFadden, eds., Structural

Analysis of Discrete Data with Econometric Applications, MIT Press, 1981).

This option is not available for the LOGIT command, but the same

results can be obtained in the binary case by saving the probabilities in

the PROB subop (as described above) and then using a SET

statement:

set xb = 1.0/(1.0 + exp(-phat))

There appear to be fewer situations where these values are useful

in logit analysis.

When the dependent variable takes more than two values, but these values

have a natural ordering, as in common in survey responses, the ordered

probit model is often appropriate. The discussion here is, of necessity,

rather brief and interested readers are urged to consult R. McKelvey and W.

Zavoina, "A Statistical Model for Ordinal Dependent Variables,"

Journal of Mathematical Sociology (1975) where the model and

estimation procedure are described in detail.

For concreteness we assume that we have a variable Y_i which takes

three different values, "low," "medium," and "high," scored one, two,

and three, respectively. (It does not matter to SST which values the

variable actually takes, since the PROBIT command will temporarily

recode values from low to high as integers.) We can think of the discrete

dependent variable Y_i as being a rough categorization of a continuous,

but unobserved, variable Y_i^*:

If we observed Y_i^* we could apply standard regression methods. For

example, we might assume that Y^* is a linear function of some

independent variables x_1i ... x_Ki plus an additive

disturbance u_i:

where u_i is normally distributed. Since

the scale of Y_i^* cannot

be determined, there is no loss of generality in assuming that

the variance of u_i is equal to one; this represents an arbitrary

normalization. Next, we specify the relationship between the

categories of Y_i and the values of Y_i^*:

The "threshold value" mu is a parameter to be estimated, as are the

unknown coefficients beta_1 ... beta_K. Setting the threshold

between the "low" and "medium" categories equal to zero is arbitrary, but

inconsequential if one of the independent variables is constant. In fact,

it is not possible to estimate the coefficient of a constant term (the

intercept) and two thresholds in the three category case: a shift

in the intercept cannot be distinguished from a shift in the thresholds.

In the general case of C categories, there will be C-2

thresholds to estimate. SST will always set the threshold

between the lowest and next lowest categories equal to zero.

Moreover, the threshold values must be ordered from lowest to

highest. If at some point during the estimation procedure the

thresholds get out of order, the maximization algorithm perturbs

the estimates enough to put them back into ascending order.

The probability that Y_i falls into the jth category is given by:

where mu_j and mu_(j+1) denote the upper and lower threshold

values for category j. If j is the low category, then the lower

threshold value is - and the upper threshold value is zero. If

j is the high category, the upper threshold value is +. The

log likelihood function is the sum of the individual log probabilities:

and the upper threshold value is zero. If

j is the high category, the upper threshold value is +. The

log likelihood function is the sum of the individual log probabilities:

Ordered probit models are estimated in SST using the PROBIT

command. The model described above is a straightforward

generalization of the binary probit model and, not surprisingly,

the same syntax works for the ordered probit model:

probit dep[y] ind[one x1 x2]

SST counts the number of categories in the dependent variable

and automatically orders the categories from "low" to "high".

Optional subops are the same for the ordered probit model as the

binary probit model with only slight modification. The number of

probabilities produced by the ordered probit model is equal to

one less than the number of categories in the dependent variable.

The omitted category is the low category. If the dependent

variable takes three values, then the user should supply two

variables in the PROB subop, and SST will store the estimated

probabilities that the dependent variable falls into the middle

and high categories in the specified variables:

probit dep[y] ind[one x1 x2] prob[p2 p3]

The probability that the dependent variable falls into the low

category can be obtained using a SET statement:

set p1 = 1.0 - p2 - p3

A similar calculation can be made for the percentage of cases

correctly predicted in the three alternative case:

set success=1; if[(p1 >= p2) & (p1 >= p3)]

set success=2; if[(p2 > p1) & (p2 >= p3)]

set success=3; if[(p3 > p1) & (p3 > p2)]

set success=(success==y)

freq var[success]

The more alternatives, the more tedious this calculation becomes.

Typing can be reduced by defining a macro to perform this procedure

(see Chapter 8).

The PRED subop can be used to compute beta' x_i. The

threshold values are not considered part of

beta' x_i and only one variable

should be specified in the PRED subop regardless of the number of

categories of the dependent variable. Coefficients and the

covariance matrix can be stored using the COEF and COVMAT subops.

The thresholds are stored as the last elements of the coefficient

vector and correspond to the last rows and columns of the

covariance matrix. The ROBUST subop also is allowed for the

ordered probit model.

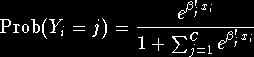

When the dependent variable takes more than two discrete

values, but these values have no natural ordering, then the

unordered logit model can be tried. In this model one category

is chosen as the "base" category. It will be seen that it makes

no real difference which category is chosen, so SST picks the low

value of the dependent variable as the base category. To be

specific, we assume the categories are numbered 0 , 1 ... C, with

zero the base category. The odds of an observation falling into

category j relative to category 0 are given by the ratio of the

probabilities:

The unordered logit models takes the log of the odds ratio above

to be a linear function of some independent variables

X_1i ... X_Ki:

The key feature of the model is that a set of K coefficients is

estimated for each odds ratio. Thus if there are K independent

variables and C+1 categories, then a total of KC coefficients

will be estimated. A little algebra shows that according to this

model the probability that the dependent variables falls into

category j is given by:

for j= 1 ... C. The probability that Y_i equals zero (the base

category) is given by:

If we define beta_0 to be a zero vector, then we see that the

probability that Y_i equals zero is also encompassed by the

previous formula. In particular, a change in the base category

so that category j becomes the new base category will mean that

the new coefficients for category k are the differences between

the old coefficient values (beta_k) and the old coefficients of the

new base category (beta_j).

The unordered logit model has attained some popularity in sociology because

of its usefulness in modelling interactions in contingency tables. If the

independent variables consist solely of dummy variables for categories of

other discrete variables and various interaction terms, then the unordered

logit model corresponds to the log Linear model for contingency table

analysis. See S. Fienberg, The Analysis of Cross-Classified

Categorical Data, MIT Press, 1981, for an introductory treatment of these

models and related issues.

The log likelihood function for the unordered logit model is given by the

product of the probabilities for each case taking its observed value:

where beta_0 is a K vector of zeroes and each of the remaining

beta_j is a K vector of parameters to be estimated.

Since the number of parameters grows with the number of

categories in the dependent variable, users may want to consider

grouping categories of the dependent variable which do not occur

frequently.

The syntax for the ordered logit model is identical to that

for the binary logit model:

logit dep[y] ind[one x1 x2]

Probabilities can be saved by specifying variable names in the

PROB subop. The number of variable names specified should be one

less that the number of categories in the dependent variable.

Coefficients can be saved with the COEF subop. Coefficients are

grouped according to which odds-ratio they pertain to. If there

are K independent variables, the first K coefficients correspond

to the log odds of choosing category 1 versus category 0, the next K

coefficients to the odds of category 2 versus category 0, and so

on. The covariance matrix, which can be saved with the COVMAT

subop, is ordered in the same way. ROBUST is also an allowable

option.

The Tobit model was proposed by James Tobin ("Estimation of Relationships

for Limited Dependent Variables," Econometrica, January 1959) for

analyzing censored regression problems. For example, in an expenditure

survey, relatively few households will report purchase of an automobile in

any particular period and hence will have zero expenditure for this

category. It may be reasonable to assume that each household has a desired

level of spending on automobiles (which is unobserved), but that no

purchases occur until the desired level of expenditure exceeds some

threshold. The observed expenditure level is either zero (if desired

expenditure falls below the threshold required to transact) or the desired

level. We do not assume that the threshold is known, but it is known

whether each observation is censored or not. Zero values of the dependent

variable correspond to censored observations while positive values

correspond to actual transactions.

The Tobit model also fits within the general regression framework. Let

Y_i^* denote the unobserved latent variable which is subject to

censoring. We assume that Y_i^* is generated by a linear combination of

the independent variables x_1i ... x_Ki plus an error u_i

which is normally distributed with mean zero and variance sigma^2:

Y_i^* is observed only if Y_i^* exceeds some threshold. Again there

is no loss of generality in assuming that the threshold equals zero since

any shift in the threshold value can be absorbed into the intercept. Let

Y_i denote the observed variables and suppose censored values of

Y_i^* have been coded to zero (in the TOBIT command, unlike the

other limited dependent variable commands, SST does care how the

variable is coded). Then:

The probability that Y_i^* < 0 is given by:

The conditional distribution of Y_i^* given that Y_i^* > 0 is given

by the following probability density function:

where phi(.) denotes the standardized normal density function:

Combining the above expressions, we obtain the sample log likelihood function:

The difficulty in maximizing the Tobit log likelihood occurs because

of the presence of sigma^2. SST computes a starting value for

sigma^2 based on user-supplied starting values for

beta_1 ... beta_K. If you do not supply starting values

SST computes an initial regression to obtain better starting values.

Poor starting values can cause the Newton-Raphson algorithm to

diverge more frequently in Tobit than most other maximum

likelihood procedures.

The TOBIT command maximizes the above log likelihood using an

iterative non-linear optimization algorithm. If censored values of

the variable y have been coded equal to zero, Tobit estimation

can be accomplished by giving the command:

tobit dep[y] ind[one x1 x2]

The options to the TOBIT command are similar to those for the other

limited dependent variable commands. The user may specify one a variable

for the censoring probabilities (1 - PHI(beta' x_i )) in the

PROB subop, while beta' x_i can be stored in a variable

specified in the PRED subop:

tobit dep[y] ind[one x1 x2] prob[phat] pred[xb]

Coefficient estimates can be saved using the COEF subop and the

covariance matrix with the COVMAT subop. The coefficients in the

TOBIT model include, in addition to

beta_1 ... beta_K, the

disturbance variance sigma^2, which SST automatically

appends to the end of the

coefficient vector and as the last row and column of the covariance

matrix.

Further details on Tobit and related models may be found in a

survey paper by T. Amemiya, "Tobit Models," Journal of Econometrics

(1984).

A popular method for analyzing choice behavior in economics in the

random utility model. The essential idea of the random utility models

is that each decisionmaker faces a choice between C alternatives,

each of which has an associated utility index describing the

attractiveness of the alternative to the decisionmaker. Utilities

are unobservable, but decisionmakers reveal their preferences by

choosing the alternative with the highest utility index. This is

the utility maximization hypothesis. The random utility model

also relies on a regression framework by assuming that the

unobserved utility values are determined by a regression-like

equation. We assume that the utility of alternative j for

decisionmaker i is given by a linear function of the independent

variables x_1i ... x_Ki plus an additive disturbance:

For example, the choices facing the individual might be choice of

transportation mode: bus or train. The factors affecting an individual's

utility for that mode might be the cost of transit on the mode and

the amount of commuting time required if the mode is chosen. Thus

the independent variables would be "cost" and "commuting time". For

each mode and each individual, we would have measures of the variables

"cost" and "commuting time" associated with the transit mode and

individual.

The probability that an individual chooses alternative j is given by:

Once a joint probability distribution is specified for the disturbances

u_i1 ... u_iC, then the likelihood function will be determined

and estimation can proceed in the usual manner. One choice of distribution

would be the normal, but in this case the computations turn out to be

rather time-consuming. Daniel McFadden ("Conditional Logit Analysis of

Qualitative Choice Behavior," in P. Zarembka, Frontiers of

Econometrics Academic Press, 1973) proposed the type I extreme value

distribution as a distribution for the errors. This distribution is

particularly convenient, since the probability that an individual picks

alternative j is then given by:

where Y_ij is a dummy variable equal to one if individual i

chose alternative j and equal to zero otherwise.

(The same probabilities could also be generated by the unordered

logit, which demonstrates the essential connection between these two

models.) The likelihood function is then the product of the

individual choice probabilities:

The multinomial logit log likelihood is globally concave in the

parameters and generally easy to maximize.

The estimation of random utility models is greatly simplified in SST.

The dependent variable is assumed to take C distinct values, ordered

from lowest to highest. There are K sets of independent variables,

each containing C different variable names which are specified in the

IVALT subop. The user provides a label for each set of independent

variables that will be used to identify the estimate of the coefficient

associated with those variables in the MNL output. Using the

transportation mode choice example discussed above, let mode equal zero

if "bus" is chosen and equal one if "train" is chosen. We also have

data on "busfare", "trainfare", "bustime" and "traintime" reflecting

the costs and amount of time for each individual and each mode:

mnl dep[mode] ivalt[cost: busfare trainfare commut: bustime traintim]

The labels "cost" and "commut" are printed with the output to identify

which variables correspond to the parameter estimates. These are just

labels used for printing and have no other purpose. SST assume that the

dependent variable for the MNL command will be coded with values

that are in the same order as the associated variable in the IVALT

subop. Thus, since the value of "mode" for "bus" is lower than that for

"train", the variables associated with "bus" should precede those for

"train" in the IVALT subop. The number of variables following each

label in IVALT should be the same as the number of alternatives or

categories in the DEP variable.

SST allows users to supply their own log likelihood functions using the

MLE command. The MLE command is much slower than the

preprogrammed maximum likelihood procedures, so it should only be used

for problems that do not fit within any of the models described above.

To use the MLE command, you will need to obtain the derivatives

of the log likelihood with respect to each parameter in the model and

then to specify these using the DEFINE command. For purposes of

exposition, we will illustrate the procedure using a normal linear

regression model:

Y_i = alpha + beta x_i + u_i

where u_i has a normal distribution with mean zero and variance

sigma^2. If x_i is non-random, the density for Y_i is:

The log likelihood for a sample (Y_1 ... Y_n) of size n

is given by:

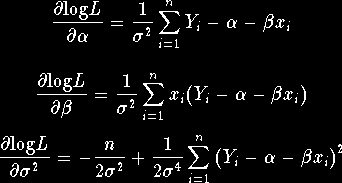

The partial derivatives of log L with respect to alpha,

beta, and sigma^2 are given by:

The maximum likelihood estimator is found by setting these partial

derivatives equal to zero and finding a solution to the equations.

In this case, of course, a closed-form solution to the likelihood

equations is available, but in general it will be necessary to

resort to an iterative non-linear procedure to solve the likelihood

equations. The method used by SST was proposed by E. R. Berndt,

B. H. Hall, R. E. Hall, and J. A. Hausman, "Estimation and Inference

in Nonlinear Structural Models," Annals of Economic and Social

Measurement (1974).

The log likelihood function and its derivatives are normally specified

using the DEFINE statement. The log likelihood function is a sum of

@(n@) terms, one for each observation. We specify the likelihood and its

derivates in terms of the contributions from each observation. For the

example above, suppose data on the variables x and y have

already been loaded into SST. We would give the commands:

define llk(a,b,s2) = -0.5*log(6.28) - 0.5*log(s2) - 0.5*(y-a-b*x)^2/s2

define ga(a,b,s2) = (y-a-b*x)/s2

define gb(a,b,s2) = x*(y-a-b*x)/s2

define gs2(a,b,s2) = - 0.5/s2 + 0.5*(y-a-b*x)^2/(s2*s2)

Once you have defined the log likelihood and its derivatives, you can ask

SST to maximize the likelihood. The log likelihood is specified in the

LIKE subop, its derivatives in the GRAD subop, and a list

of parameters is specified in the PARM subop:

mle like[llk(a,b,s2)] grad[ga(a,b,s2),gb(a,b,s2),gs2(a,b,s2)] \

parm[a,b,s2] start[0.0,0.0,1.0]

The order in which the gradients are given in the GRAD subop should

be the same as the order in which the parameters are specified in the

PARM subop. We have supplied starting values in the START

subop. If no starting values are specified, SST will use zero as a

starting value for each parameter by default. In this case, using zero

as a starting value for the parameter s2 (sigma^2) would cause

a division by zero and the MLE command would abort. Starting values

are very important for the MLE command. Good starting values

speed up the procedure; bad ones often cause the algorithm to fail.

All maximum likelihood procedures share a common set of options that

control the maximization algorithm and output.

Users can supply

starting values in the START subop. The number of starting values

should correspond to the number of parameters in the model. (In

the case of MLE, the number of parameters is equal to the number

of parameter names specified in the PARM subop. For other

procedures, consult the description above). When starting values

are not specified by the user, typically zeroes are used instead.

The criteria used to determine whether the algorithm has converged

depends on a quadratic form in the gradient of the log likelihood

function with matrix equal to the negative of the inverse of hessian.

The default convergence criteria is set at 0.001. To set the

convergence criteria at another value, include the CONVG

subop with a value of your own choosing. For example:

probit dep[y] ind[one x] convg[0.0001]

would set a more stringent criteria for convergence.

By default, the maximum likelihood routines continue for a maximum

of fifteen iterations. To increase (or decrease) the iteration

limit, include the MAXIT subop. For example:

logit dep[y] ind[one x] maxit[50]

would allow SST to continue for up to fifty iterations.

At each iteration, SST normally picks a direction to search in the

parameter space and attempts to pick the optimum stepsize for taking

a step in this direction. Occasionally, the program will fail to

find a stepsize which will increase the likelihood and will

report a convergence failure. You may force SST to take a fixed

stepsize of your own choosing at each iteration by including the

STEP subop which takes as its argument a positive number:

tobit dep[y] ind[one x] step[1.0]

With the above command, SST will use a stepsize of one at each

iteration.

If SST has difficulty achieving convergence, it is a good idea to

increase the amount of information that the program prints at each

iteration using the PRT subop. The default level of printing

is one and includes the value of the likelihood function at each

iteration, stepsize, and the convergence criteria. To have SST

print out the covariance matrix after the last iteration, increase

the print level to two. To have parameter values output at each

iteration, set the print level at three. A common problem is

incorrectly specified derivatives. SST will calculate numerical

derivatives and print them on the first iteration if you set the

print level at four. For example:

mnl dep[y] ivalt[constant: one one x: x1 x2] prt[4]

will produce the maximum available output.